Anatomy of a Legal Acquisition

We studied 4,172 mergers and acquisitions and distilled three insights on how founders exit their companies. So, what is peculiar?

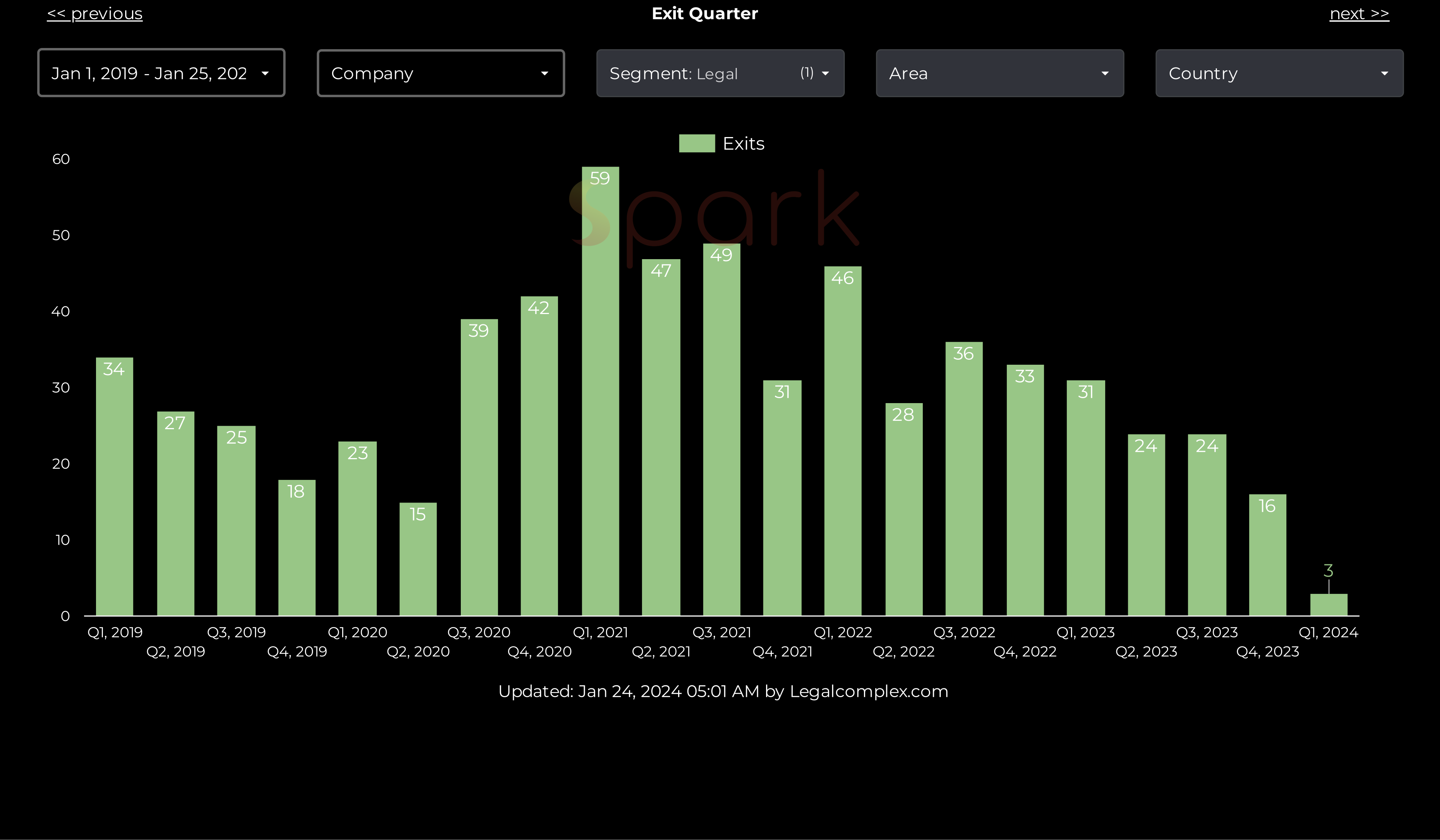

This week we released our Mergers and Acquisitions (M&A) numbers. You can find the download links at the bottom of this post. In 2023, the most dramatic stat was the 85% drop in total transaction value. Furthermore, our analysis revealed M&A activity has been decreasing since 2023. Now, when you hear so-called experts say, ‘We’ll see more consolidation,’ remember: that is a lazy statement trying to look smart. However, despite the dramatic drop in transaction activity and value, one other peculiar trend caught our attention.

Acquisition Targets

First, let’s answer a straightforward question: Why would one acquire a legal tech enterprise? Looking at the 95 deals we registered, here are three insights that we could deduce from all:

- Acquisitions are mainly driven by targets, talent, or technology, in that order;

- Targets refer to customer bases that help boost the balance sheet with a robust ARR (Annual Recurring Revenue);

- Talents achieve the best outcomes through bootstrapping, as any outside funding makes them vulnerable to lockups;

None of the points above should be shocking for anyone. Indeed, acquiring a company that has already done the hard work is the fastest way to gain a fresh set of attractive customers.

Consequently, companies accomplished this by either being a better seller or building a better product. This leads us to question whether this was a talent or technology play. Now come the handy insights for founders: did you really build the fastest car, or are you just an excellent driver? Because once a founder has been in the driver’s seat, it’s almost impossible to get comfortable as a passenger.

Acquiring Tech & Data

We continue our tradition of not naming names. Yet, we can manage two examples to illustrate what looks healthy to us.

3E, a provider of chemical compliance solutions, has acquired Chemycal, a 7-person regulatory monitoring shop based in Rotterdam. Additionally, Chemycal aggregates chemical and product compliance data from over 1,500 sources and maintains a library of substances and materials to keep customers updated. Thus, the acquisition combines 3E’s expertise in environmental, health, safety, and sustainability compliance with Chemycal’s global regulatory monitoring capabilities.

The private equity firm Thoma Bravo is acquiring the German software company EQS Group, which specializes in compliance and investor relations software, for €400 million. This acquisition price, marking a 53% premium over EQS’s previous stock price, indicates that the deal is likely to be completed. Despite EQS being a relatively small public software company, this move has led TechCrunch to ponder whether compliance tech represents a good startup bet.

Adding Debt

Ultimately, this brings us to the reason you probably clicked on this analysis: DocuSign. It was first reported on December 15, 2023, that DocuSign was working with advisers to explore a sale. According to the Wall Street Journal, it could potentially be one of the largest leveraged buyouts in recent times. While debating this on LinkedIn, one thing dawned on me: why private equity (PE)?

As always, there is an upside and a downside. Notably, Private equity firms offer founders and owners a generous way out of their businesses. The downside: a private equity acquisition is not the same as Facebook buying Instagram or Google buying YouTube. The Financial Times reported that private equity firms often resort to buying back companies after IPO flops. If you wonder why private equity buy companies, check our Power post. The TL;DR: private equity firms are investment vehicles that enable high returns for their investors. And they are able to achieve that by fancy financial engineering.

This perhaps explains why private equity firms acquire companies with little to no prior venture capital (VC) investment. After examining M&A transactions we have registered, it’s clear the majority of companies acquired by PE do not have any VC capital. Even when a PE-backed company goes on a shopping spree, they actively avoid VC-backed companies. Very peculiar.

You can download the M&A report here and schedule a chat for a one-on-one deep-dive.