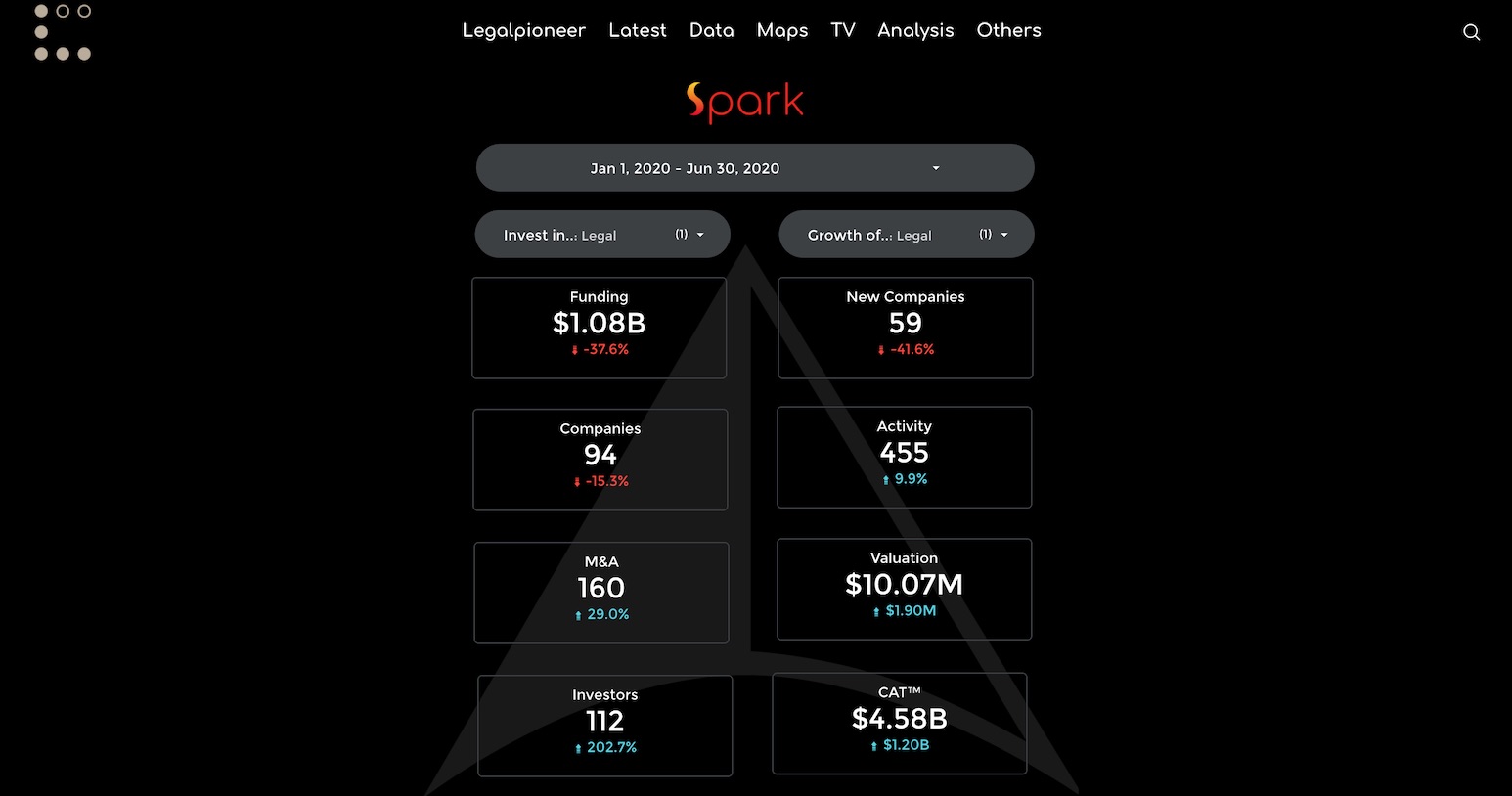

The Surface: $1.08 Billion in 2020 Legal and Tax Funding..so Far

On the surface, breaking a billion in the first half of 2020 looks healthy for legal and tax. Yet, if we peel away May, it is a different picture.

TLDR: The legal market is currently operating in a financial distortion field. May stimulus is masking recession-resistant companies. However, tech-infused services fared better than traditional text & talk consulting services. New applications in Risk Tech offer new opportunities for Legal Tech.

Credit

No, credit isn’t a new catalyst, rather a warning from the ‘Rebound’ analysis. One reason we surpassed a billion was Litigation Finance: Parabellum Capital donated a sizable chunk to the overall tally. Check our views on Litigation Funders as Legal Tech in this twitter spat. What’s remarkable is the fact that taken over a six-month period, companies usually eclipsed litigation funds in round sizes. It is perhaps a sign we’ve entered borrowed time.

Now as everyone is slowly running out of cash, most will have to turn to credit. We noted that about 14% of the top US Legal Tech companies took advantage of the Payroll Protection Program (PPP). We didn’t mention that, while doing the analysis, we encountered numerous traditional law firms and justice programs in the list of grants. Justice programs aren’t surprising because it’s rare to find those with a commercially viable business model. Most are born addicted to grants. As for business models: you may recall we encouraged everyone to listen to Kim Kardashian-West. Moreover, the US only released the recipients of over $150k loans, so we’re only seeing the surface.

In contrast, none of our top 25 Dutch legal tech companies were mentioned in the NOW loans report (Dutch stimulus program). Similar to the US, we did see several law firms and legal service providers in the NOW list of recipients. In any case, Legalcomplex is sticking to the mantra: numbers before names, that is why we won’t mention any names. However, these developments demonstrate the robustness of tech-fused services versus traditional talk & text consulting services. So ‘Starting in Legal Tech‘ may have become just a little more attractive.

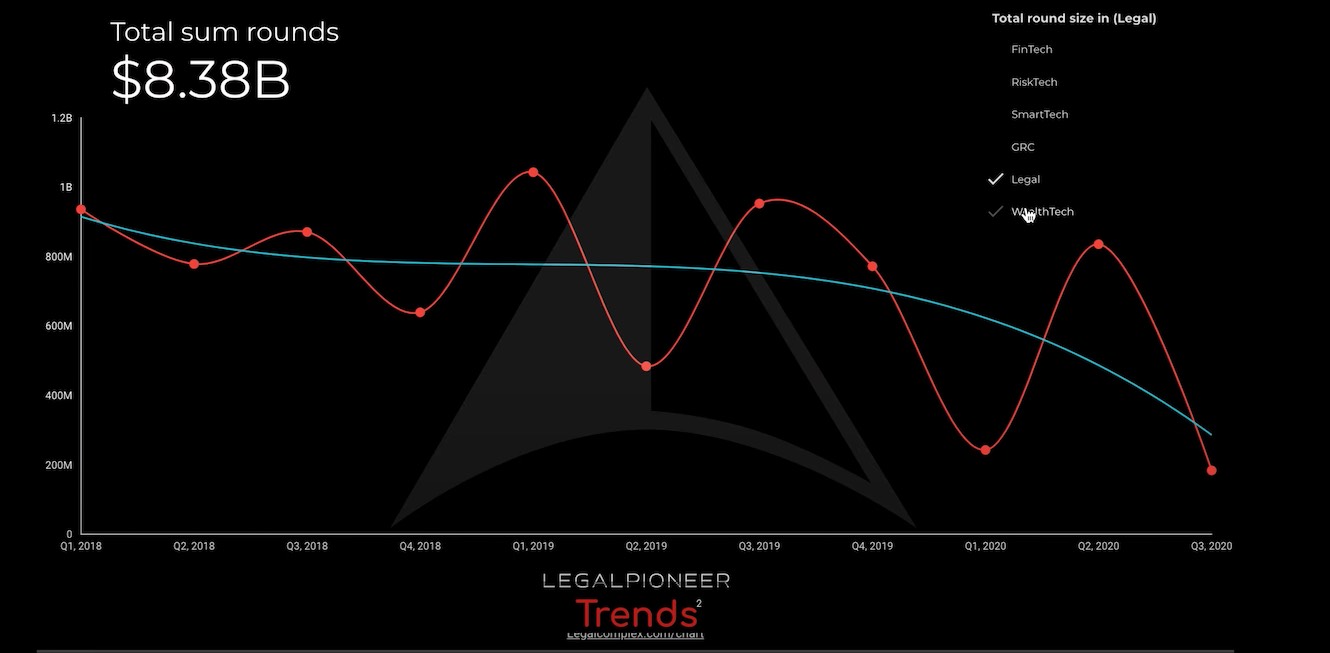

Not only did we noticed a shift in where money was allocated but also when it was distributed. Most of this year’s action happened in May which brought in $644 Million. We initially registered SirionLabs in May, but they technically completed the round in April. In contrast, as far back as 2017, we notice that January and the summer months as the time the big rounds come around.

In short: there is a distortion in the market with so much stimulus flooding the economy. It’s hard to calculate how recession-resistant most businesses in the legal industry really are. Especially since we’re still dealing with Corona aftershocks and the second wave.

Conflict

Back to the numbers: $1.08 billion is lower than in previous years. Both 2019 and 2018 had outliers in the first half of the year like Legalzoom, Seal Software, and Onit. Clio happened in the second half of 2019 and doesn’t count in this summary.

This brings us to the conflict: our data reveals mega-rounds aren’t the beginning but rather the end of a trend. These numbers happen when the internal company metrics match up with external perception. These events initialize a final push for a monopoly in a certain space.

Moreover, the innovation capital coming into the legal market isn’t always invested in the players we all recognize. How can we spot the competition? This question led us to analyze ‘Who Are Your Challengers‘. To illustrate, check the Contract 2020 chart above with players in FinTech and SmartTech we excluded in the $1.08 Billion breakdown.

While most see mega numbers as an acknowledgment of a growing market, it’s actually an unreasonable assumption. Meaning, more money doesn’t equate to more market but rather results in less competition. We noticed a correlation between major rounds and subsequent drop in funding for new ventures in those niches. That’s why we sometimes end up in a conflict with legal industry experts. These conflicts stem from the source of knowledge: data versus past experiences or surveys. While these sources are complementary to data, they can be contradictory. Ultimately, when some get wowed by the bang, we’ve already seen data on the ignition.

Case in point: Safehub uses the Internet of Things (IoT) to warn companies to impending earthquakes. Businesses need this to proactively protect their operations and employees (RiskTech). At some point, they can use this model to warn citizens at home as well (CivicTech). And when they scale, they’ll become the benchmark for real estate value (FinTech) in whatever region suffering from tremors. Think tremors are only felt along fault lines? Read this cautionary tale on real estate in Groningen, The Netherlands from The New York Times (EcoTech). At that point, we’ll need a Seismic Witness (LegalTech) similar to Orbital Witness for legal conveyance. Safehub is taking the commercially more sustainable route to Legal. Both companies raised rounds this July, only one counted to the Legal & Tax wrap-up.

..and that is why we chase the Spark and not the bang.

Overview first half 2020 in Legal & Tax

Overview first half 2020 in Legal & Tax